Dynamic Monitoring Illuminates the Insurance Blackout Period

For decades, Canadian insurers have operated with limited visibility into their policyholders’ lives between policy inception, renewal and claims. This “blackout period” has made it difficult to anticipate risk, detect early signs of attrition and proactively engage customers.

While insurers may have internal tools to initiate customer engagement, they typically receive limited data on policyholders — until a claim is filed or a policy is cancelled. In today’s volatile economic and regulatory environment, this reactive model is no longer sufficient.

Why the blackout period matters more than ever

Consumers are under pressure — high interest rates, rising unemployment and inflation are straining household budgets. At the same time, insurers are grappling with:

- Record-breaking CAT losses (e.g., $8.5B in 2024)

- Regulatory shifts (e.g., Bill 47, climate risk guidelines)

- A substantial increase in insurance shopping and demographic shifts year over year

These stressors are converging to create a more dynamic and risk-sensitive market. As a result, leading insurers should consider moving beyond static, point-in-time assessments and adopting continuous monitoring to help stay ahead of risk and retain valuable customers.

Dynamic credit monitoring: A strategic advantage

Using TransUnion® CreditVision® Insurance Risk Score and examining changes in a consumer’s credit profile, we analyzed how changes in credit behaviour over a 12-month period correlate with key insurance events — such as cancellations, claims and shopping activity. The findings revealed three leading indicators that can help insurers proactively manage risk and improve retention.

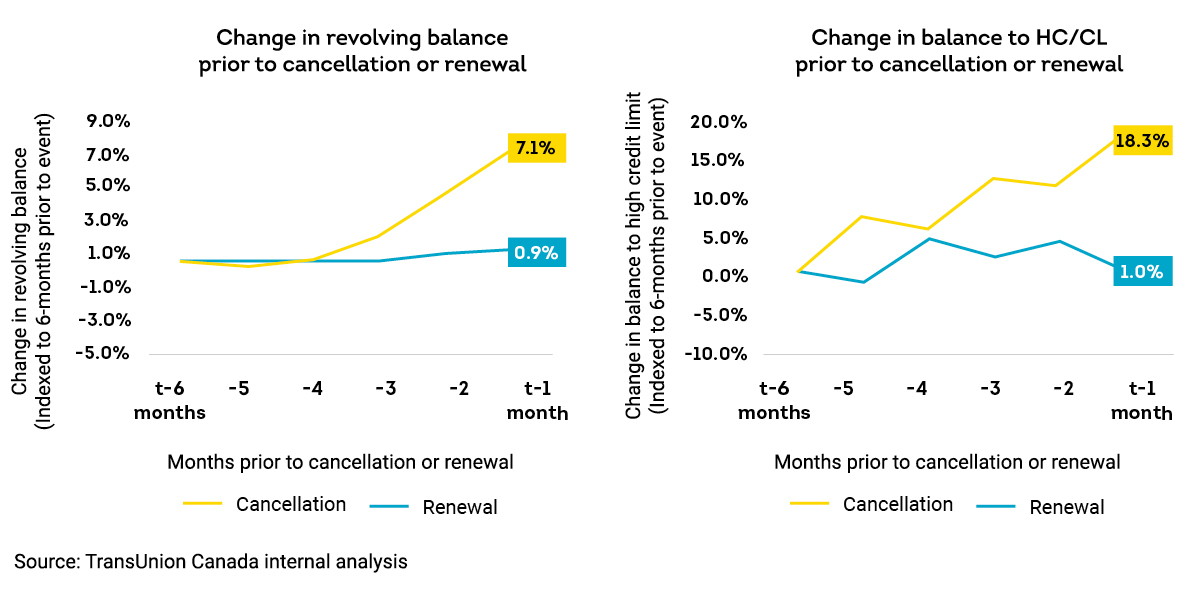

1. Changes in balances and credit utilization

Consumers experiencing financial strain often show:

- Rising revolving balances (7%+ increase over six months)

- Higher balance-to-limit ratios (18%+ increase)

These shifts are strong predictors of cancellation risk and may also signal increased claims risk as financially stressed consumers may defer vehicle or house maintenance or seek opportunistic claims.

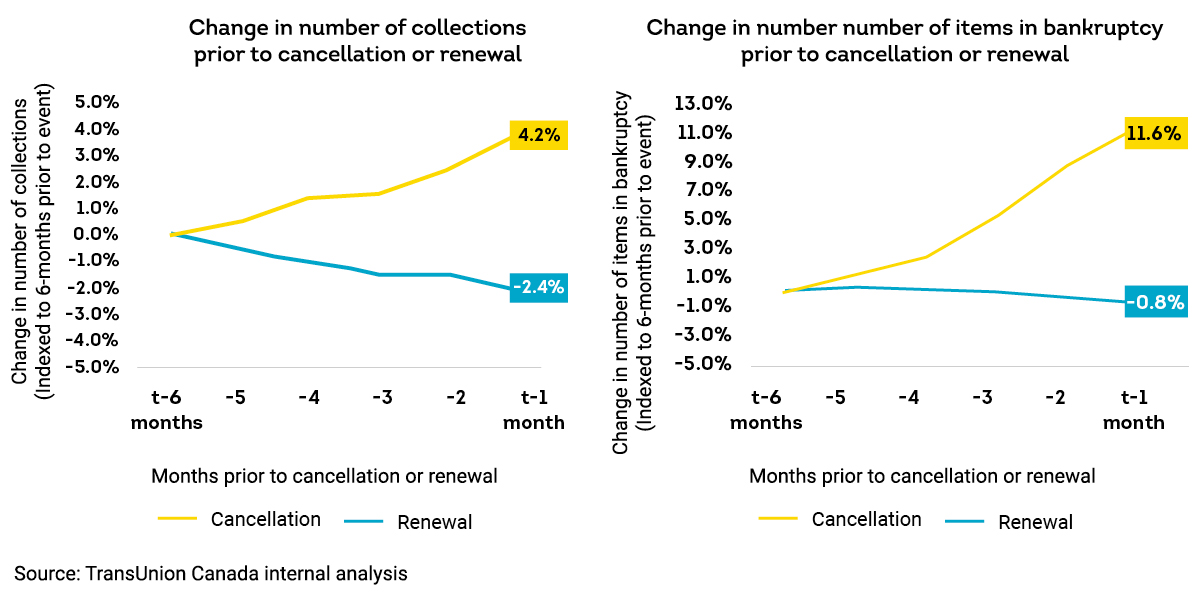

2. Tradeline management and payment patterns

Closures of credit accounts — especially auto loans — or a decrease in monthly payments can indicate deeper financial distress:

- Increase in collections → elevated claims risk

- Decrease in average monthly payments → even stronger signal of increased claims risk

- Account closures-> leading indicator of both cancellation and claims

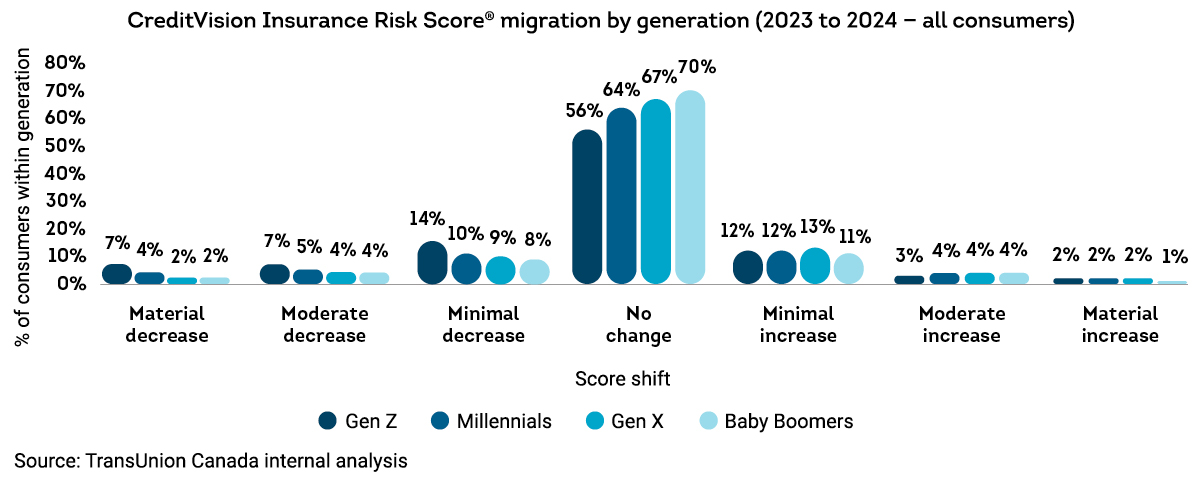

3. Risk score migration

While overall portfolio risk appears stable, 15% of policyholders experienced material shifts in risk within a year. These were especially pronounced among Gen Z and Millennials who are more financially volatile.

* Minimal Shift --> score shift +/-1 decile

*Moderate Shift --> score shift +/-2 or more deciles

This means insurers relying solely on policy inception data are missing critical changes in risk, as well as opportunities to intervene or tailor premiums and coverages accordingly.

From insight to action: What insurers can do

Dynamic monitoring:

- Helps insurers identify at-risk customers before they cancel or claim

- Supports the deployment of targeted retention strategies (e.g., flexible payment plans, coverage adjustments)

- Helps enhance pricing accuracy by incorporating real-time risk changes

- Optimizes the detection of potential fraud through behavioural red flags (e.g., sudden balance spikes)

✅ Strategic recommendation: Integrate Dynamic Monitoring into mid-term reviews or renewal workflows via batch or real-time APIs.

Conclusion: Illuminate the blackout, position your business for growth

In a market defined by economic uncertainty and rising consumer expectations, insurers should evolve from reactive to proactive. By leveraging Dynamic Monitoring, insurers can:

- Reduce cancellations and claims

- Improve customer lifetime value

- Help to build trust through timely, relevant engagement

The blackout period doesn’t have to be dark. With the right data and strategy, it can become a window of opportunity.

Learn more about the CreditVision Insurance Risk Score.

Contact Us

We're sorry, your request failed. Please try again in a little while.